Financial Management & Digital Banking: A New Proposition (Part 2)

Millennials’ Needs & Demand

Previous chapter: Part 1: Background and Market Research

What kind of digital banking service and savings product that millennials need and desire?

A digital maelstrom: a perfect brew with millennials’ purchasing power, shift in lifestyle choices and growth in digital e-commerce

Millennials, which represent one third of the total Indonesia population and will make up approximately 44% of Indonesia’s productive age (15–64) in 2030, is one important force that may lift growth higher. They comprise as the largest workforce, command the largest portion of the income, and correspond to unique blend of higher value consumption; which more toward experiences rather than functional needs.

Being a mobile first and mobile only generation, the combination of millennials’ rising consumption pattern, increase in disposable income, and stellar rise of digitalisation can provide further opportunity to raise Indonesia’s overall private consumption growth. But at the same time, this also becomes a perfect chance for e-commerce players to capitalize this opportunity by providing a convenient, highly accessible online shopping experience with fast shipping and good customer experience. This in turn drives a consumptive lifestyle that promotes instant gratification, encouraging millennials to focus the enjoyment of “now” rather than spending carefully to ensure the safety of future savings.

With this lifestyle in mind, millennials are more attracted to banking products that incentivises and supports their consumptive lifestyle (ex: products with features cash-back, promo and discounts, etc). This is especially dangerous because it promotes a mindset and lifestyle that is beneficial only for short term, and preventing them to switch for a more sustainable and healthy lifestyle.

Financial mindset: Spend first, Save later

Based on the research by Telstra observing millennials on eight different countries (Millennials, Mobiles & Money): it is evident that across all geographies, Millennials are great ‘Spenders’. The ‘Spender’ to ‘Saver’ ratio among the Millennials is 2:1. Millennial ‘Savers’ are usually seen on their mobiles during late evenings. Insights such as commonly active times of the day and repeat browsing patterns on mobile can help guide strategies to maximise reach and engagement. They can also be used to lead customers from simple transactional behaviour to the more consultative and higher value wealth-creation saving services.

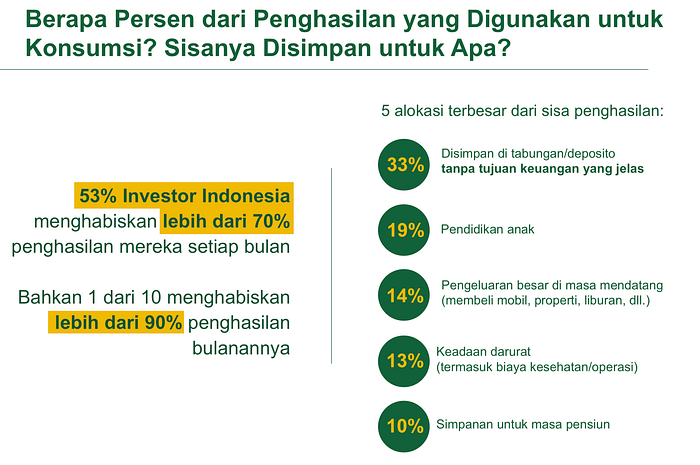

As stated in KOMPAS’s article “Fintech” dan Perilaku Keuangan Generasi Milenial”: This consumptive lifestyle trend is reflected in the OJK data at the end of 2015, shown by a decreasing Marginal Propensity to Save (MPS) ratio and the increasing Marginal Propensity to Consume (MPC) ratio. The MPS ratio itself has been below the MPC ratio since 2013. This indicates that since a few years ago more people spent their income on shopping activities compared to saving money. This was confirmed by the Manulife Investor Sentiment Index in Q4 2015 which revealed; 53 percent of respondents spend 70 percent of their income shopping, and 10 percent of respondents spend 90 percent of their income shopping.

The weak culture of saving from an early age will reduce the chance of the millennial generation to accumulate wealth, which they should be able to enjoy when they are no longer productive and unable to work anymore.

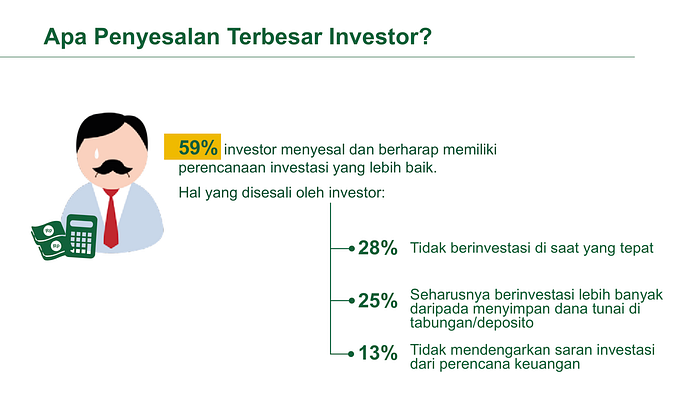

The Manulife Investor Sentiment Index survey said 60 percent of respondents said they wanted to be able to control spending better, but did not have adequate tools or tools, while 53 percent of respondents said they regretted not preparing their financial plans early on. This insight will be explored further in the section”Naively too optimistic and no plan for investment: an insecure plan for future” below.

Lack of financial literacy and preparation: not knowing how to utilize and maximize financial services for wealth creation

From the research literature I gather, even the banked, digitally savvy segments still sees banking as a way to manage their income and spending, just as a means for survival and manage their practical needs (put their income into saving account, use it to pay daily and monthly bills, loans, mortgage, etc).

This is reflected on the breakdown of the financial activities that “advanced-active use” customers do on regular basis, which is to save aside money, receive wages, paying bills, loans and other transactional / transfer activities.

Even in the saving products, Indonesians still see saving accounts as a way to only cover regular expenses (basic necessities) and for emergency funds. This may be caused by:

- the low level of financial literacy

- lack of understanding for the use of bank accounts

- lack of trust and understanding for digital methods

- preference for cheaper, better suited informal alternatives, and perhaps for group saving mechanism (such as koperasi, arisan, etc)

It’s a very limited, short-term view of banking as a service because they don’t see it as a way to improve their lives and achieve their life goals and purpose (with the exception for mid-term goals such as savings for education, child savings, and house / car mortgage). There is still lack of awareness and understanding that financial service can also be used to not just manage their financial basic needs, but can also be used for a wider and longer purposes that can enrich their lives. For example, as an investment tool to create savings for their pension plan, create a diversified portfolio that enable them to live with a passive income, for wealth creation, etc.

Naively too optimistic and no plan for investment: an insecure plan for future

I also looked into investment sector because of an interesting finding based on HSBC’s report The Future of Retirement, Shifting Sands:

Indonesian millennials expect to be able to retire earlier at 56 years old, faster than the current average retirement age (61 years old), and therefore, they need to obtain more robust financial supports from previous generations.

And yet, as stated in Manulife’s survey in 2017 ( Survei Manulife: Investor Indonesia Menganggap Enteng Pengeluaran di Masa Pensiun): Indonesian investors have a high risk due to not being ready to face the financial reality in retirement later. Manulife Investor Sentiment Index (MISI) found that almost all investors (96%) believe they will continue to have the same lifestyle as now or even better in retirement later, without realizing that their savings will continue to shrink due to spending in retirement, and will endanger his finances.

Why they are at risk:

- The majority of investors are too optimistic about their future, with 71% of investors confident that they are on the right track to achieve a variety of financial goals, and even 10% of investors believe they will exceed the target. Conversely, only 19% of investors are worried that they will run out of money later in retirement.

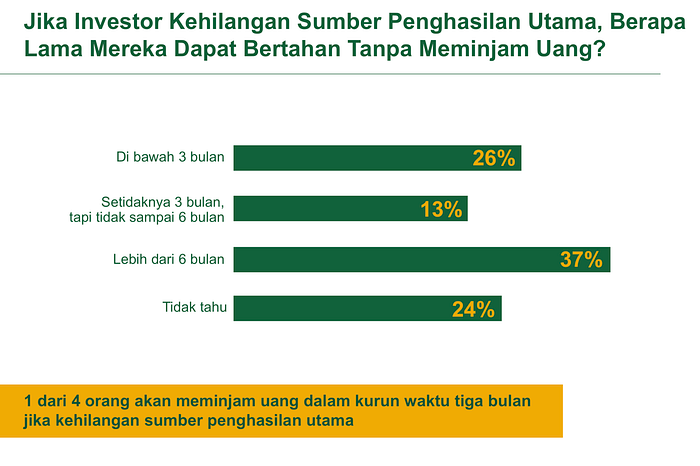

- Despite the optimism of investors to achieve their savings targets, they have not taken adequate steps to protect their financial future. Although investors place retirement planning as one of the main financial priorities, ranked second after children’s education, nearly a quarter of investors (24%) allocate less than 10% of their savings for retirement savings. In addition, many (57%) expect to collect savings for retirement of a maximum of Rp 100 million, which will be exhausted within two to three years — taking into account their current average household expenditure of Rp 4 million per month.

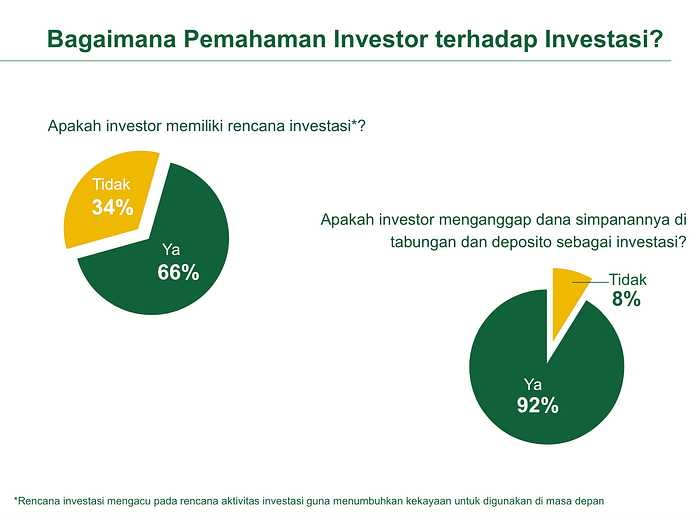

- Investor’s hesitation to take risks also limits their ability to accumulate wealth. Nearly three-quarters (74%) of Indonesian investors prefer low-risk investments. This can be seen from the increasing sentiment towards cash funds, from 71% in Q4 2015 to 88% in 2016. By placing the majority (60%) of pension funds in non-investment products that offer low risk but provide low returns, most investors (65%) feel confident that they have diversified their portfolio sufficiently.

In conclusion, the factors that cause investors’ failure in optimizing their investment:

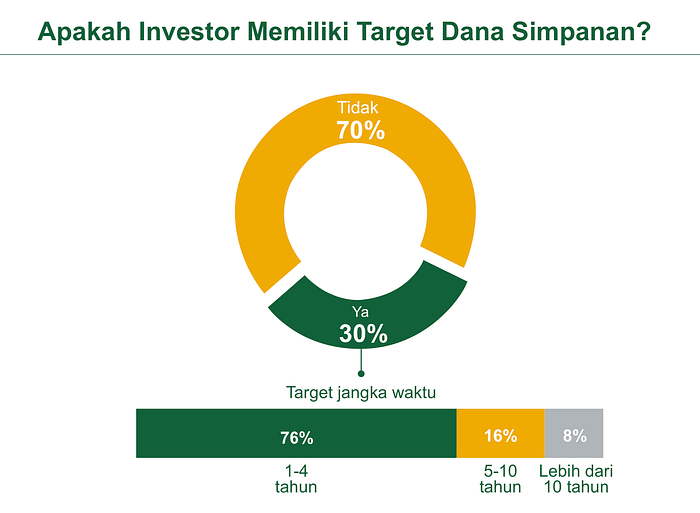

- Lack of financial planning and monitoring that will enable them to control their spending and manage their savings and investment according to their target (at the same time, 70% of the respondents also did not set a target amount for their investment)

2. Lack of financial knowledge and literacy, which caused them:

- not knowing the right timing, method and products to maximize their investment

- to over estimate the return they gain from those products

Conclusion: The behaviour, needs and demands of Indonesian Millennials

Lifestyle and consumption behaviour:

- Overall, millennials could spend up to 50% (vs. the preceding generation, up to 30%) of their disposable income towards the so-called 4S: Skin, Sugar, Sun, Screen

- This higher consumption level is driven by strong economic development, increase in disposable incomes, preference in spending on “experience” services/products and the growth of e-commerce businesses that provide a fast and convenient online shopping experience.

Lifestyle and consumption behaviour:

- Big on spending and saving, though they are more likely to give a larger proportion of their income to spending instead of saving. This mindset drives them to go for financial products that can support their lifestyle

- Wants to control their spending so they can save better and allocate more to their investment

- Expect to be able to retire earlier at 56 years old, faster than the current average retirement age (61 years old), and they expect to be able to enjoy the same or even better lifestyle in their retirement.

- Knows the importance of investment for their future, but it’s hard for them to commit because of the distant and intangible nature of this goal (pension and retirement fund). Furthermore, millennials are too optimistic about their ability in securing sufficient retirement fund. This is caused by:

- their underestimation on the effort and amount needed for a sufficient retirement fund,

- their lack of understanding on investment products (they think savings and deposit accounts can be used for investment, and they don’t know the best methods to diversify their portfolio and maximise their wealth)

- over estimation on the return they gain from those products

- Lack of financial knowledge and literacy hinders millennials’ ability in utilising and maximising the necessary financial services to accumulate wealth and invest for their future.